/cases endpoint. You can manage disputes by performing tasks such as submitting a dispute, retrieving information such as dispute status, and uploading supporting documents.

This page provides information on the dispute process and best practices. For information on how to manage disputes in the Marqeta Dashboard, see Disputes in the Dashboard. For specific details on how to integrate with the Mastercard or Visa network, see Managing Mastercard Disputes or Managing Visa Disputes. For reference information, see Disputes (Mastercard), Disputes (PULSE), or Disputes (Visa) in the Core API reference.

Note

The dispute process is the same for both virtual and physical cards.

The dispute process is the same for both virtual and physical cards.

What is a dispute?

A dispute is a request or process to have a transaction charged back to the cardholder. A dispute is often initiated if a cardholder:- Did not receive a product or service.

- Did not recognize the charge or business name on their statement.

- Believes the product to be damaged, defective, or not as described.

- Was the victim of fraud, card theft, or identity theft.

Best practices

The following are best practices for resolving your disputes and optimizing your win rates:- When a card is reported lost or stolen, immediately deactivate the card to ensure a tight timeline between a lost card and potential transactions. Submit the dispute case immediately after the dispute has been opened by the cardholder.

- If your team is working directly with cardholders, create a dispute form or use an example from Marqeta for gathering as much information as possible along with the cardholder’s attestation of the dispute.

- Provide the strongest possible level of documentation, such as communication with the merchant, receipts, and timelines. Incomplete dispute information or lack of documentation can decrease the likelihood of winning a dispute.

- If the dispute involves goods and services issues with a merchant, have a representative of your company or the cardholder first contact the merchant directly, which can result in a refund and make a dispute unnecessary.

Note

No more than 15 fraud-related disputes can be initiated against the same primary account number (PAN, also known as the card number).

No more than 15 fraud-related disputes can be initiated against the same primary account number (PAN, also known as the card number).

Before initiating a dispute

Before you initiate a dispute, advise the cardholder to contact the merchant directly to resolve the issue. If the issue cannot be resolved, begin the dispute process by initiating a dispute case. You must submit a dispute even if the amount does not meet the program’s dispute threshold. Have the cardholder complete a dispute form and submit that form with any supporting documentation that might assist in the dispute review process, such as receipts or email communication with the merchant. Incomplete dispute forms or insufficient details increase the likelihood of losing the dispute.The dispute lifecycle

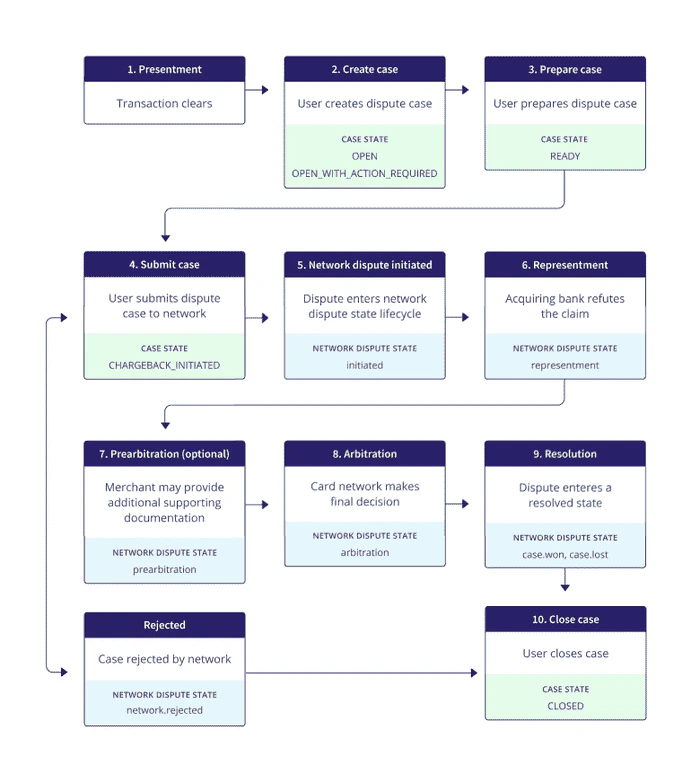

Once the cardholder has contacted you indicating their intention to dispute a transaction, the 30-day SLA timeline for compliance begins. Disputes are required to follow a series of steps defined by the card networks and participating banks. You start the process when you create a dispute case. As you define the dispute details, the dispute is tracked by dispute case states. After you submit a dispute case to the network, the dispute is tracked by the network using network dispute states. The following diagram shows the overall lifecycle, including dispute case states and network dispute states.

Presentment: The transaction clears. This is a typical transaction clearing event. In order for there to be a dispute, the transaction must first clear.

Create case: The user creates a dispute case to dispute the transaction on behalf of the cardholder, beginning in the

OPEN or OPEN_WITH_ACTION_REQUIRED state.Prepare case: The user assembles the necessary information to prepare the dispute at the network. When all the information and supporting documents are assembled, the dispute case progresses to the

READY state.Submit case: The user submits the dispute to the network. The dispute case state transitions to

CHARGEBACK_INITIATED. If the dispute case is rejected, it enters the network.rejected state and exits the dispute lifecycle. Review the dispute case to determine if it can be resubmitted.Network dispute initiated: The dispute enters the network dispute lifecycle in the

initiated state. The acquiring bank can respond to the dispute directly or forward it to the merchant. If forwarded to the merchant, the merchant can accept the loss or provide documentation to refute the dispute claim.Representment (Second Presentment): The acquiring bank attempts to refute the claim, likely because they believe it is invalid or incomplete. Merchants have recourse to defend against the claim by submitting a representment. For example, if a cardholder claims fraud in a card present transaction, the merchant may provide the card network with a representment that includes a signed copy of the receipt. In this case, the merchant has complied with their requirements and is not liable. The dispute enters the

representment state.Prearbitration: Upon receipt of the representment, Marqeta may choose to reach out to the acquiring bank once again. Visa refers to this additional step as prearbitration. This optional step allows the merchant an additional opportunity to provide supporting documentation. The dispute enters the

prearbitration state.Arbitration: All information and supporting data has been provided to the network and the network makes a decision. The network’s decision is final and must be accepted by both Marqeta and the acquiring bank.

Resolution: After arbitration, the dispute is resolved and enters into either the

case.won or case.lost state.Note

The vast majority of disputes are resolved during the Initiated state. Disputes typically take 30-120 days to resolve. A dispute is won if the acquirer does not respond to the dispute within the expected timeline. Expected timelines vary according to the card network, which are defined in their respective 30-day service level agreement (SLA) timelines. For the Visa SLA, see Managing Visa Disputes.

The vast majority of disputes are resolved during the Initiated state. Disputes typically take 30-120 days to resolve. A dispute is won if the acquirer does not respond to the dispute within the expected timeline. Expected timelines vary according to the card network, which are defined in their respective 30-day service level agreement (SLA) timelines. For the Visa SLA, see Managing Visa Disputes.

Disputes under threshold

To ensure that all disputes are visible and meet the regulatory compliance, you must submit a dispute even if it does not meet the program’s dispute threshold. It is mandatory for Managed by Marqeta (MxM) programs that are on Marqeta’s regulatory platform to submit all disputes, even if they are under threshold. When you submit such a dispute, it is processed as follows:Case is moved to a

Marqeta informs cardholders of the status of the case based on the communication process.

If you manage cardholder communications, you are responsible for informing cardholders.

CLOSED state and a case.won resolution, without submission to the network.

Marqeta informs cardholders of the status of the case based on the communication process.

If you manage cardholder communications, you are responsible for informing cardholders.

Note

For customers whose cardholder notifications are not managed by Marqeta, you must implement additional logic to handle the provisional credit webhooks based on the dispute amount. For more information about webhook updates, reach out to your Marqeta representative.

For customers whose cardholder notifications are not managed by Marqeta, you must implement additional logic to handle the provisional credit webhooks based on the dispute amount. For more information about webhook updates, reach out to your Marqeta representative.

States and transitions

Case states indicate the status of a dispute case as you prepare it before submitting to the network. Network disputes states represent the current state at the network. Case transitions move the dispute through the dispute case states on the Marqeta platform. Once a dispute case has been submitted to the network, the dispute progresses through the network dispute lifecycle and is tracked using network dispute states. Transitions move a dispute through the resolution process by moving the dispute to the next state. Case transitions move the dispute through the dispute states; network dispute transitions move the dispute through the network dispute states.Dispute case states

Dispute case states include the following. TheOPEN, OPEN_WITH_ACTION_REQUIRED, and READY states are staging states where information can be gathered and other concerns addressed. The CHARGEBACK_INITIATED state formally starts the dispute process at the network.

| State | Description |

|---|---|

OPEN | The dispute case was created. |

OPEN_WITH_ACTION_REQUIRED | The dispute case has been created with an action required. |

READY | The dispute case is ready for review. |

CHARGEBACK_INITIATED | A dispute was initiated at the network. |

CLOSED | The dispute case was closed. |

Network dispute states

Once a dispute has been initiated, it flows through a series of states, or transitions. The following are the states involved in a dispute case resolution:- Initiated

- Representment

- Prearbitration

- Arbitration

- Case won

- Case lost

- Network rejected

Initiated

After presentment, the dispute enters theinitiated state. The request is reviewed and the dispute initiated with the card network as follows:

- Depending on the reason for the dispute, Marqeta applies a provisional credit to the cardholder’s account.

- If additional information or documentation is required, Marqeta requests this information from you.

- You are notified when the dispute is initiated.

Representment

If the acquiring bank attempts to refute the claim, the merchant can defend the claim by submitting a representment, also known as the dispute response. The dispute then enters therepresentment state. For example, if a cardholder claims fraud in a card present transaction, the merchant could provide proof that the card was swiped and show that they have a copy of the receipt signed by the cardholder. The merchant has then complied with the card network requirements and is not liable.

Marqeta reviews the representment:

- Marqeta may request additional documentation from the cardholder in order to resubmit the dispute case to the card network.

- Marqeta resubmits the dispute case, if appropriate.

Prearbitration

The dispute case enters theprearbitration state if Marqeta chooses to reach out to the acquiring bank once again after the dispute has entered representment. Marqeta may submit updated information to support the dispute.

Prearbitration allows the cardholder and the merchant to provide further information about the dispute. It also allows the cardholder to submit a second dispute if the initial dispute was rejected. Prearbitration and the Prearbitration Response can take up to 30 days for each part of the process. For the Visa lifecycle, prearbitration proceeds differently, with different timelines, for Allocation or Collaboration disputes.

For detailed information about the timelines for prearbitration, see Mastercard resolution timeframes or Visa resolution timeframes.

Note

Only relevant dispute cases assume this status.

Only relevant dispute cases assume this status.

Arbitration

The dispute case enters thearbitration state when the acquirer disputes a claim, and the issuer submits the case to the card network for arbitration. In arbitration, the card network decides who wins the dispute case.

Case won

If the dispute is won by the cardholder, it enters thecase.won state. Marqeta completes the following actions:

- If a provisional credit was not issued at the time when the dispute was initiated, the customer’s account is credited for the amount of the dispute.

- If a provisional credit was issued at the time when the dispute was initiated, no further action is required.

Case lost

If the dispute is lost by the cardholder, it enters thecase.lost state. Marqeta completes the following actions:

- If a provisional credit was issued when the dispute was initiated, the provisional credit is reversed by debiting the customer’s account in the amount of the dispute.

- If a provisional credit was not issued when the dispute was initiated, no further action is required.

Network rejected

If the card network rejects the dispute submission, the dispute enters thenetwork.rejected state in which case the dispute amount may be written off by either the issuer or the program or resubmitted with updated details. For guidelines for reducing network rejections, see Best practices.

Resolving disputes

Additional considerations for resolving disputes include notifying the cardholder of the dispute outcome and managing provisional credits, reconciliation, mitigation, and true-up transactions.Notifying the cardholder

Once a dispute is resolved, notify the cardholder of the outcome. Example email templates are provided below for both the case won and case lost scenarios.Note

These templates are provided for your reference and convenience. Communication of outcomes to cardholders is your responsibility.

These templates are provided for your reference and convenience. Communication of outcomes to cardholders is your responsibility.

Case won email template

The review of the transaction you disputed on[DATE] has been completed. We are pleased to report that the dispute has been resolved in your favor and your account has been credited for the disputed amount.

- Dispute details: XXXXX

- Amount of the credit to your account: XXXXX

- Date of the credit to your account: XXXXX

Case lost email template

The review of the transaction you disputed on[DATE] has been completed. We regret to inform you that the dispute has been resolved in favor of the merchant. The provisional credit to your account, if any, has been reversed.

- Dispute details: XXXXX

- Original transaction amount: XXXXX

- Amount of the provisional credit reversal adjustment to your account: XXXXX

- Date of the reversal: XXXXX