Innovative propositions designed to serve specific communities are a rapidly emerging trend in fintech. There are literally no limits to use-case diversity. Take, for example, Rizq*. Branded the ‘UK’s first Sharia-compliant, ethical digital banking app’, its recent launch demonstrates how modern technology is capable of working seamlessly with the tenets of one of the world’s great religions.

To better understand how payments pioneers are harnessing fintech solutions to serve the specialised banking needs of different communities, Marqeta spoke to Peter Trebelev, Rizq’s co-founder and head of business development.**

How did you get started in fintech and what was the inspiration behind Rizq?

I’d been interested in fintech for a few years, as it’s at the forefront of innovation in our economy and I’m fascinated by how it’s changing the way people relate to money. I managed to get a position with a fintech company and used this time to learn more about how businesses are structured and operate. Whilst there, I constantly consulted with another member of our team as we were both interested in launching our own venture. And so, we set to work thinking of a proposition. We both felt that there was no point in trying to recreate the likes of Monzo or Revolut, given how far ahead they are in the market, so we decided to consider catering to a specific audience.

In late 2019, we started analysing the potential of different communities, areas, and ideas, including a student-facing neobank focusing on cashback deals, for example. However, it was around this time that we met Rizq’s third founder, who is a Muslim, and this led to the idea of developing a digital banking solution that would better meet the needs of Britain’s Muslim population. The more we looked into it the more it made sense, because the digital banking market isn’t really developed in this area and the incumbents are quite traditional. Thus Rizq was born and we launched the company in February of 2020.

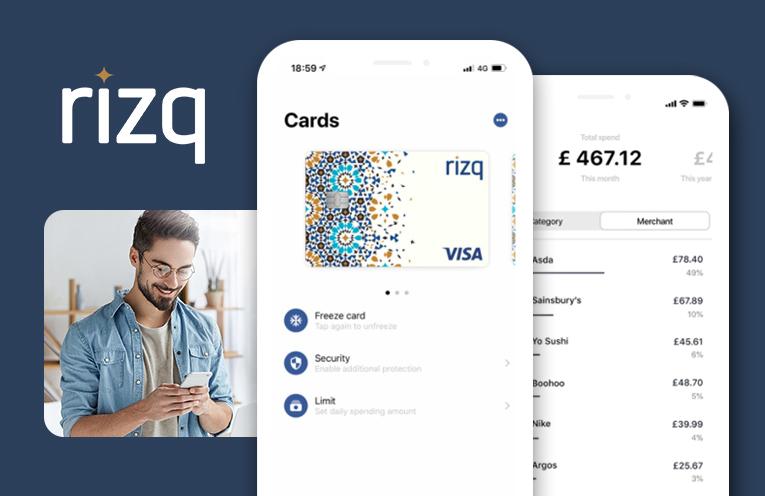

Can you tell us a bit about what Rizq offers and where you’re heading in terms of products and features?

As well as offering modern accounts with debit cards and an app to retail and business customers, Rizq is designed to meet a range of our audience’s needs. For example, many of our customers need to make remittances to Islamic countries. Rizq aims to let them do this at a very competitive FX rate. We’ve included a ‘giving’ feature that allows account holders to make donations to their favourite good causes – all within 10 seconds or less. Alongside this, customers are able to take advantage of ethical cashback and discount offers that align with their beliefs.

But ultimately, we see Rizq as a lifestyle app that is designed to help people seamlessly manage a whole range of activities that require financial transactions. We’re currently launching the Rizq Marketplace, which will become a hub for vendors across a range of services, such as travel, financing, pensions, sharia wills services, and more.

It sounds like you’ve made real effort to learn about your audience. Can you tell us how you’ve gone about gaining insights to inform your development?

Firstly, we regularly send out questionnaires and reward people for their responses to ensure a big enough sample on survey topics. We’ve also made a point of going to events. For instance, we visited a Halal Food Festival and spoke to lots of potential customers and prospective merchant partners. These data points have helped to inform the development of our B2B product – it was really important to understand what they needed from an application. We also use our intuition – because customers don’t always necessarily know what they want, so testing features by putting them in front of our audiences and seeing how people respond has been really helpful. Finally, there’s the commercial consideration. Is a feature going to drive income or be a loss leader? In the early stage of your growth, it’s important to prioritise revenue generation and positive marketing implications over iterations that might only be taken up by a small percentage of users.

Can you describe what impact the COVID-19 pandemic has had on Rizq?

We launched in February 2020 during the early part of the pandemic. We were lucky in the sense that we didn’t need to restructure or switch from an office to a home working situation. However, there were still challenges. For example, in the early stage of a startup, you need to talk to lots of people, so that was tricky. Also, recruiting team members was difficult because we were unable to meet candidates face to face, which is something you really need to do in order to get people to understand the company culture. That said, we are a digital first business and if there were to be another major emergency, we would be ready to pivot given the experience we’ve gained.

You mentioned that you had looked at launching a student product. Are there learnings from Rizq that could translate into other propositions?

Yes, and for this reason we’ve set up RizqLAB. We want to help others who are embarking on a similar path to ours. I think there’s an opportunity to develop lots of exciting propositions, as there are lots of underserved groups out there and what we’ve found is that your target audience really appreciates it when you build something specifically for them – word quickly spreads and drives uptake. From a product perspective there are lots of overlaps, such as in regulation and compliance and the infrastructure for issuing, processing, safeguarding, etc. The key is in developing the USPs and the right branding. RizqLAB has the potential to help businesses go to market in the quickest and most cost effective way possible, bypassing a lot of the R&D and set-up expenses, through a licensed approach.

Finally, what are you looking forward to most in the year ahead?

Rizq Marketplace is a personal responsibility of mine so I’m very excited about taking that forward. We also really want to elevate the charity element and make a positive impact on the community. RizqLAB has a lot of potential too, based on the conversations we’re developing at the moment. Looking at the broader landscape, fintech is booming on a global level and there are lots of opportunities. Some countries are already incredibly advanced while others are still developing. It’s a really exhilarating sector to be in and I see Rizq establishing itself as a digital banking leader among the British Muslim community and beyond – but also as a service provider and specialist in the fintech industry. The Muslim community in the UK may be a small but growing one, but beyond it there are 2 billion people globally – with many of these people demanding fair access to banking services (and rightly so, as this is imperative for them to build up credit scores, manage their money, and more). Rizq’s overall aim is to help them do this, be it through Rizq or other brands.