Opening up the payment flow has become imperative for modern card issuing, yet this is a capability not all card issuing platforms offer. One reason for that chasm is that for decades, financial institutions have used ISO 8583, the international standard for facilitating the flow of transaction information.

Essentially, ISO 8583 requires developers to strictly adhere to the entire transaction payment flow. With the movement towards API and modern card issuing capabilities, it’s allowed an issuer to be more proactive in the authorization flow process. With modern card issuing, authorization happens through ingesting the ISO data string and translating it into a readable JSON format with separate fields and expanded results, ultimately delivering a legible structure to our customer’s endpoint, clearly laying out each piece of transaction detail.

This flexibility allows card program owners to have the ability to read and better understand the transaction elements in question, as well as combine it with their own data to make informed authorization decisions. Additionally, a memo field, such as a loan or invoice number, can be added to the authorization response to help with reconciliation down the road.

This increase in control means that you can have greater impact on your authorization rates and ultimately your program’s profitability.

In this post examining takeaways from the white paper, “Understanding card issuing platforms,” we explain the basics of payment card processing, and describe how Marqeta’s API makes it possible to open up payment flow while still complying with ISO 8583. As your business begins creating your request for proposal (RFP) for selecting the best card issuing platform for you, we encourage you to ask the following questions:

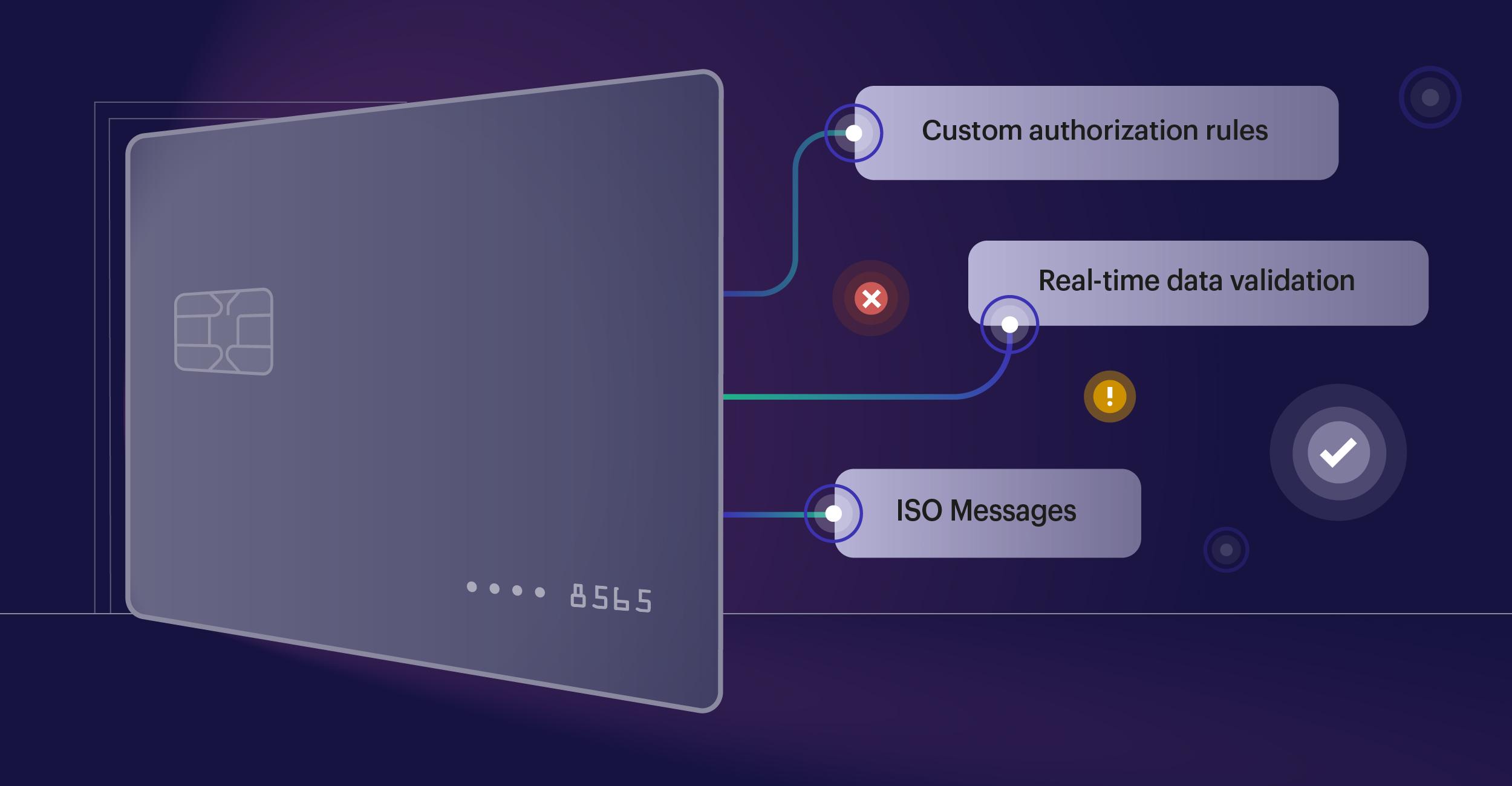

- Will you be able to customize authorization rules for your particular business or vertical?

- Is real-time data validation for authorizing transactions possible, even for a transaction based on dynamic pricing?

- Will ISO 8583 messages be parsed and translated to a simple format, like JSON before pushing them to your system endpoints?

- Can your system both receive and send data in real time to the card issuing platform?

If creating custom payment experiences, new digital banking products, and embedded finance applications are important to your business, the answers to these questions will have great value. They’ll indicate whether your business will have the benefit of an open payment flow, which opens a world of possibilities.

Payment processing 101

Payment flow for electronic payments involves a payment network and four other major players: the cardholder, merchant, acquirer processor and issuer processor.

To facilitate the flow of transaction information between a processor and the issuer, a card network (for example, Visa or Mastercard) is involved. The “four parties” exist on top of the card network, which is not a “party” itself. Networks provide the underlying infrastructure, communications, standards, and processes to facilitate financial transactions across geographic boundaries by passing information and funds between processors and issuers. In return, they charge the payment processors and issuers with a license or card scheme fee. These networks also set the standards that processors and issuers must follow for communication, dispute resolution, and other processes.

Cardholder – Receives a card from an issuer and uses it to initiate a payment to a merchant.

Merchant – Aspires to accept card payments in exchange for goods or services. To ensure that the cardholder can pay and the merchant can receive, the merchant requests authorization for a payment transaction on that card. To accept these types of payments, the merchant must open a merchant account with a payment processor to settle the funds.

Acquirer Processor – Provides the merchant the core technology to accept electronic payments, and facilitates the transaction between a merchant and the card network. Using the appropriate card network, the processor captures the transaction information and forwards it to the issuer (or issuer processor) for approval. When the transaction is approved by the issuer, the payment processor also settles the funds with the merchant along with all the related fees.

Issuer Processor – Provides the core technology to enable processing of transactions through relationships and integrations with one or more bank identification number (BIN) sponsors. They also manage payment authentication and information about the cardholder. For a payment to be successful, the issuer processor is responsible for checking that:

- The transaction is valid

- The card belongs to a valid and trusted cardholder

- The cardholder has enough funds (or credit) to make this payment

Opening up payment flow

While the ISO 8583 standard has evolved over time to accommodate emerging technologies, it still presents limitations that could stifle innovation. This contributed to Marqeta’s development of the open API for the payment card. Marqeta’s API breaks up a linear payment flow into many well-defined pieces. This is what we mean by opening up the payment flow. It empowers businesses to validate and authorize card transactions against dynamic data while still meeting ISO 8583 obligations.

By opening up the payment flow, modern card issuing platforms open a doorway to a world of potential customization that allows businesses to align their payment experience with their unique business rules. For instance, you can validate and authorize card transactions to limit a card’s use to a certain dollar amount, frequency of use, merchant ID, merchant category code, permissible time and date of use, the geolocation of the cardholder at the moment of transaction or their risk profile, among many other factors.

DoorDash is among the many businesses that benefited from customization. Their challenge was how to enable their Dashers to pay for individual orders while reducing the risk of fraud. With transactions happening every second, each with a different amount and at a different restaurant, a traditional payment card would only be able to verify the identity of the driver. DoorDash needed tight controls around each transaction, including limiting the card’s use to a certain dollar amount and merchant category code.

Open payment flow is an important differentiator

Not all card issuing platforms are created equal. The ability to open up the payment flow represents a key difference for businesses to consider when selecting a card issuing platform that truly enables you to customize payment experiences.

For more best practices for building an RFP, see the Marqeta white paper, “Understanding card issuing platforms.” It can start you down the path toward outlining your current and future use cases, and mapping out a payment authorization flow and an expected behavior of the payment experience. Or if you want to talk to an expert, we are happy to help.